In a landscape where many borrowers feel the pressure of rising interest rates and stricter underwriting, it can be surprisingly easy to find lenders willing to extend credit even when your score is on the lower end. Recent data from CNBC’s “Easiest Personal Loans” list shows that several institutions are tailoring their offers for folks with fair or poor credit, and they’re doing so with a blend of technology‑driven speed and flexible terms.

Who Are the New Frontiers in Personal Lending?

The 2026 edition of CNBC’s personal‑loan roundup spotlights three standout lenders: Avant, Upstart, and Marcus by Goldman Sachs. Each brings a distinct approach to underwriting, but they share one common goal—making cash flow easier for borrowers who may not fit the classic “prime” profile.

- Avant specializes in short‑term personal loans and has a reputation for approving applicants with credit scores as low as 550. The company relies heavily on alternative data points, such as bank account activity, to gauge repayment risk.

- Upstart uses machine learning algorithms that consider factors like education level, employment history, and even the borrower’s industry to predict default likelihood. Their minimum score requirement sits around 620.

- Marcus by Goldman Sachs, while traditionally a more conservative lender, has expanded its offering to include unsecured personal loans for scores down to 600. Marcus emphasizes transparency in fees and rates.

Each of these lenders offers loan amounts ranging from $1,000 up to $25,000, with terms between six months and five years. While the interest rate bands are still above prime levels, borrowers can often secure a rate that is competitive relative to their credit profile.

Speed and Convenience: The “Next‑Day” Promise

A key selling point for many applicants is how quickly they can receive funds after approval. Avant’s platform boasts an instant decision process—most approvals are delivered within minutes of the application, and if submitted before 5:30 p.m. ET on a weekday, funds may be deposited by the next business day. This rapid turnaround can be a lifesaver for unexpected expenses such as medical bills or car repairs.

Upstart also emphasizes speed but adds an extra layer of security. Their algorithm reviews credit history alongside other signals before pushing a decision to the borrower. While not always instant, most applicants see results within 24 hours, and funds are typically available shortly thereafter.

Marcus, on the other hand, adopts a slightly slower process that prioritizes thoroughness. Applicants can expect an approval decision in one to two business days, with disbursement following promptly once all documentation is verified.

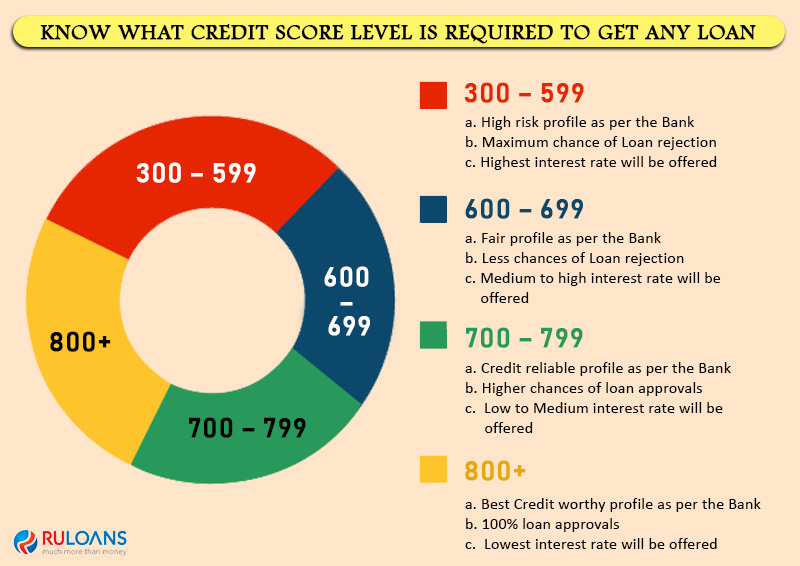

How Credit Scores Influence Terms and Rates

Even within the “easiest” category, credit scores play a pivotal role in determining both interest rates and loan terms. Below is a quick snapshot of how typical lenders structure their offers based on score ranges:

| Credit Score Range | Typical APR | Loan Amount | Term Length |

|---|---|---|---|

| 550‑599 | 15%–22% | $1,000 – $5,000 | 12 – 36 months |

| 600‑649 | 13%–18% | $2,500 – $10,000 | 12 – 48 months |

| 650‑699 | 11%–16% | $5,000 – $15,000 | 18 – 60 months |

| 700‑749 | 9%–14% | $10,000 – $25,000 | 24 – 72 months |

| 750+ | 7%–12% | $15,000 – $30,000 | 36 – 84 months |

The table illustrates that borrowers with scores in the 600‑649 range can still secure reasonably competitive rates, especially when they choose a lender that leverages non‑traditional data. It also highlights how loan amounts tend to increase with higher credit scores—a reflection of lenders’ confidence in repayment.

Why Alternative Data Matters

Lenders like Avant and Upstart have turned to alternative data—information not captured by traditional credit bureaus—to assess risk more accurately. Examples include:

- Bank account balances and transaction patterns that indicate consistent income flow.

- Rental payment history, which can be a strong predictor of future loan repayment.

- Employment stability, gauged through payroll data or LinkedIn activity.

By incorporating these signals, lenders can offer credit to borrowers who might otherwise be excluded. This trend is part of a broader movement toward more inclusive financial services, where “creditworthiness” extends beyond the four-digit score that dominates headlines.

The Role of Fees and Grace Periods

While interest rates are the headline figure, borrowers should also scrutinize fees that can erode savings. Common fee types include:

- Origination Fees—often a percentage of the loan amount, ranging from 1% to 5%.

- Late Payment Penalties—charged when a payment is missed or late; some lenders waive these for the first month.

- Pre‑payment Penalties—though rare, certain loans may charge a fee if you pay off the balance early.

For instance, Avant typically charges an origination fee of 2% and offers a 10‑day grace period for late payments. Upstart does not impose pre‑payment penalties but includes a small administrative fee for each payment that falls outside the scheduled date. Marcus prides itself on no pre‑payment fees and transparent disclosure of all costs upfront.

Grace Periods: A Cushion in Tight Times

A 10‑day grace period can be a lifesaver, especially when cash flow is unpredictable. It allows borrowers to avoid late fees while still meeting the lender’s expectations. However, it’s important to note that this buffer does not extend the loan term; missing payments beyond the grace window will affect your credit score and may trigger additional penalties.

Real‑World Impact: Stories from Borrowers

Consider Maria, a 34‑year‑old teacher who had a 620 credit score due to an old medical debt. She needed $4,500 for a home renovation. After applying with Avant, she received an instant decision and a loan offer at 16% APR—significantly lower than the 25% she’d expect from a payday lender. With a 36‑month term, her monthly payment was manageable, and the loan helped her avoid higher‑cost options.

John, a freelance graphic designer with a 580 score, turned to Upstart for $3,000 to cover business expenses during a slow season. Despite his low score, Upstart’s algorithm approved him at 18% APR after evaluating his consistent gig work and education background. He repaid the loan in 24 months, improving his credit profile over time.

What These Stories Reveal

The common thread is that these lenders view credit through a broader lens. They assess risk not just by past borrowing behavior but also by current financial habits and future earning potential. For borrowers who have made a few missteps but maintain steady income, this approach can unlock opportunities that were previously out of reach.

Choosing the Right Lender for Your Situation

When evaluating lenders, consider the following checklist:

- Credit Score Compatibility: Ensure your score falls within the lender’s accepted range.

- APR and Fees: Compare total cost of borrowing, including hidden fees.

- Loan Term Flexibility: Shorter terms mean higher monthly payments but less interest over time.

- Application Speed: If you need funds quickly, prioritize lenders with instant or next‑day approval processes.

- Customer Service: Read reviews to gauge how the lender handles disputes and customer inquiries.

It’s also wise to use online comparison tools—many financial websites offer side‑by‑side rate comparisons that factor in your credit profile. These tools can help you identify the best fit before committing to an application.

Tools That Make Comparison Easier

Financial news outlets and personal finance platforms frequently publish up‑to‑date loan listings, complete with real‑time rates and eligibility criteria. For instance, CNBC’s “Easiest Personal Loans” list updates monthly and includes links to each lender’s application portal. Similarly, Bankrate’s personal loan guide provides a searchable database of lenders, allowing you to filter by credit score, loan amount, and term.

When using these resources, keep in mind that advertised rates may be contingent on a soft credit check or a pre‑qualification offer. The final rate you receive will depend on your hard inquiry and the lender’s final assessment.

How to Prepare Your Application

Even with a lender that accepts lower scores, a well‑prepared application can streamline the process:

- Gather Documents Early: Have recent pay stubs, bank statements, and tax returns ready.

- Check for Errors: Review your credit report for inaccuracies—disputing errors can boost your score before applying.

- Understand Your Budget: Use a loan calculator to confirm you can afford the monthly payment over the chosen term.

- Ask About Flexibility: Inquire whether the lender allows early repayment without penalties or offers payment holidays if needed.

By following these steps, you reduce the likelihood of delays and increase your chances of a favorable outcome.

The Importance of Timing

Lenders often review applications in batches. Submitting during off‑peak periods—such as midweek mornings—can result in quicker processing times. Additionally, if you’re planning to apply for multiple loans (e.g., a personal loan and a credit card), coordinate the timing so that only one hard inquiry is recorded on your report.

Final Thoughts

The 2026 lending environment offers more pathways than ever for borrowers with fair or poor credit. By understanding how alternative data, speed of approval, and fee structures interact, you can make an informed choice that aligns with your financial goals. Whether you’re renovating a kitchen, consolidating debt, or covering an unexpected expense, there are lenders ready to extend a helping hand—even when the traditional credit score story isn’t in your favor.

For those looking for a lender that blends technology with personalized service, consider exploring options like Now Loan, which offers competitive rates and a streamlined application process designed to meet the needs of today’s borrowers.